The Ministry of Labor Decree #699 published in the Official Gazette #32 on the 24th July 2025 (attached a scanned copy), has raised the minimum monthly basic salary to LBP 28,000,000 and the minimum daily workers’ wage at LBP 1,300,000 effective from the 1st August 2025.

Author: citylog

MoF decision #689-1 Extension of Objection deadline on tax adjustments till 11 September 2025

The Ministry of Finance (MoF) decision #689 dated 24th July 2025, has extended the deadline for taxpayers to submit their objection on MoF tax adjustments till the 11th September 2025.

However, the taxpayers have to settle 30% of the objected tax and penalties amount to benefit from this extension.

MoF notification #2323/1 dated 11 July 2025-Electronic notifications to the taxpayers

The Ministry of Finance (MoF) notification # 2323/S1 issued on the 11th July 2025 related to the MoF electronic notifications to the taxpayers.

All taxpayers already submitting their tax returns electronically will only be notified by the MoF electronically through its website starting from the 16th July 2025.

Therefore, the MoF requests that all taxpayers submitting their tax returns electronically to check the section “Notifications” within their “Taxpayer profile” on the MoF website: www.eservices.finance.gov.lb on a regular basis for any new notifications or correspondence sent by the MoF.

عندما تتحوّل النعمة إلى علّة

![]() Article by attorney Karim Daher

Article by attorney Karim Daher

صادق المجلس النيابي خلال جلسته العامة المنعقدة بتاريخ 30 حزيران 2025، في خضم الهرج والمرج والعروض المسرحية المميّزة التي رافقت النقاش حول مسألة إقتراع المغتربين، على مشروع قانون يرمي إلى منح المتضرّرين من الحرب الإسرائيلية على لبنان بعض الإعفاءات من الضرائب والرسوم وتعليق المهل المتعلقة بالحقوق والواجبات الضريبية ومعالجة أوضاع وحدات العقارات أو أقسامها المهدّمة.

لا شك ولا جدل بأنّ إقرار هذا القانون هو ضرورة وطنية ملحّة وواجب مواطني وإنساني بديهي، نظراً للأضرار الباهظة والخسائر الفاضحة التي تكبّدتها في الأرواح والممتلكات، ولم تزل، شريحة كبيرة من أهلنا، نتيجة للعدوان الإسرائيلي الغاشم على محافظتَي الجنوب والبقاع كما ومناطق مختلفة من بيروت الإدارية والجبل وسواها من المناطق والمحافظات الأخرى الآهلة؛ وما تجلّى وترتّب عنها، بالإضافة إلى انكماش وتقلّص في النمو والنشاط الإقتصادي.

مع التذكير، إذا لزم، بأنّ تلك الظروف المأساوية وما رافقها من نتائج ومترتبات، قد ولّدت بالمقابل موجة تضامن عارمة بين اللبنانيِّين للحلول مكان الدولة العاجزة دوماً والمقصّرة غالباً، وتلبية احتياجات النازحين من إيواء ودواء وطعام ومسكن وطبابة وتموين وملبس وغيرها من الضروريات الملّحة. وقد ذكّر هذا التحرّك والمبادرة، بما شهدته العاصمة بيروت إبّان المرحلة التي تبعت إنفجار المرفأ المأساوي من تضامن وتفاعل مجتمعي جامع وداعم، أفضى إلى إقرار القانون رقم 194 تاريخ 16/10/2020 لحماية المناطق المتضرّرة بنتيجة الإنفجار في مرفأ بيروت ودعم إعمارها؛ والذي تضمن في بعض مواده إعفاءات من الضرائب والرسوم وتعليق مهل متعلقة بالحقوق والواجبات الضريبية ومعالجة أوضاع وحدات العقارات أو أقسامها المهدّمة والمتضرّرة على شكل مشابه في بعض الأحيان لما تضمّنته أحكام القانون الجديد.

لذلك، ولكل الأسباب المعروضة، لا لبس ولا التباس ولا تردّد في القول والتأكيد، بأنّ إقرار هكذا قانون هو ضرورة لا بل واجب وطني. وكنّا سبّاقين في صياغة نصّ مماثل وطرحه مع مجموعة من الخبراء الإقتصاديِّين في خضم العدوان.

غير أنّه، وإذا ما نظرنا ملياً وبدقّة إلى مضمونه وأحكامه، نكتشف أنّه يكتنفه شوائب خطيرة ومطبّات عديدة ومتعدّدة من شأنها، إذا ما أُبقي عليها من دون تعديل، أن تحرفه وتحيّده عن أهدافه الحميدة وغايته الجديرة بالثناء. لا بل من المرجّح أن تحوّله إلى أداة تسمح لجهات نافذة ومتحكّمة باستعماله باستنسابية مطلقة لغايات خاصة، ولاسيما إنتخابية، من خلال التحكّم والتمنين والتمييز؛ مع التذكير أولاً بأنّنا على مشارف إنتخابات نيابية جديدة، يُؤمل منها تغيير الواقع الزبائني والطائفي والإنتقال تدريجاً إلى دولة المواطنة والحق والقانون والمؤسسات. ناهيك عن ضرب مبدأَي العدالة والمساواة المصانَين في الدستور.

كما يقتضي أيضاً لفت النظر ثانياً إلى أنّ تمويل هذه الإجراءات والإعفاءات الملازمة سيتمّ بمعظمه من خلال القروض والضرائب (الحاضرة و/أو المستقبلية) التي يتحمّلها على حدٍ سواء ومن دون تمييز، حاضراً أو مستقبلاً، جميع المواطنين والمكلّفين المقيمين شرعياً وأصولاً على الأراضي اللبنانية.

وعليه، لعلّه من المفيد في ما يلي، على سبيل البيان لا الحصر، إستعراض جملة من الأحكام الواردة في القانون المشوبة ببعض الغموض و/أو العيوب و/أو الأخطاء، لاسيما على ضوء المقارنة مع ما تضمّنه القانون رقم 194/2020 الآنف الذكر للجهة عينها، مع التمنّي بأن يصار إلى استدراكها ومعالجتها من قبل المشرّعين أنفسهم قبل فوات الأوان.

بدايةً، لا بُدّ من التوقف عند الجهة المخوّلة درس الملفات وتحديد معايير الإستفادة وهوية المستفيدين من الإعفاءات المقترحة في القانون، التي بموجبها يُنفَّذ مشروع الإعفاءات. فبينما كان القانون رقم 194/2020 (إنفجار مرفأ بيروت) ينيط بلجنة خاصة – تضمّ ممثلين عن كافة الجهات المختصة (من وزارات ومجلس إنماء وإعمار وقيادة الجيش ونقابة المهندسين والمؤسسة العامة للإسكان والهيئة العليا للإغاثة) برئاسة ممثل قيادة الجيش – مهمّة تلقّي كافة الوثائق المتعلقة بالأضرار وتحليلها وتخمين الكلفة والتعويض والمتابعة والتأكّد من إنجاز الأعمال وإعداد تقرير يُرفع إلى مجلس الوزراء الذي يصدّق على القوائم ويُقرّر التعويض وسبل تمويله (المادتَان الثانية والرابعة)… يقلب هذا القانون الجديد المعايير ويوكل هذه المهمّة إلى وزارة المال بمفردها من خلال «لجنة تقنية» داخلية تعمل الوزارة على تشكيلها وفقاً لما ترتئيه أحادياً (المادة السابعة من القانون الجديد). على أن يجري ذلك بالتعاون مع شركة خاصة تتعاقد معها – الوزارة عينها في أغلب الظن – لتدقيق الملفات ومقاطعة المعطيات مع المؤشرات الواردة في التقرير المشترك بين البنك الدولي والمجلس الوطني للبحوث العلمية.

أي بمعنى آخر، يعود تحديد معايير الإستفادة وهوية المستفيدين إلى وزارة واحدة تابعة في ولائها لمرجعية سياسية محدّدة لها مصالح في المناطق المنكوبة والمتضرّرة، مع كل ما قد يترتّب عن ذلك من نتائج لجهة معايير الموضوعية والحيادية والعدالة والمساواة؛ وكل ذلك على مقربة من إنتخابات نيابية مصيرية.

ومن ثم لا محال إلّا أن نتوقف أيضاً عند المدة المحدّدة للإستفادة من الإعفاءات الممنوحة على جملة من الضرائب والرسوم كضريبة الأملاك المبنية ورسم القيمة التأجيرية وسائر الرسوم البلدية ورسوم المياه والكهرباء والهاتف وسواها؛ إذ إنّها تبدأ إعتباراً من تاريخ 8/10/2023 وتستمر إلى حين انتهاء أعمال الترميم وإعادة الإعمار من دون تحديد مدة قصوى (المادتَان الأولى والثالثة من القانون الجديد). وهذا ما من شأنه إطالة أمدّ إعادة الإعمار والترميم والتأثير السلبي لا محال على العمران والتخطيط وشكل واستدامة الأحياء والقرى؛ مع ما يستتبع ذلك من نتائج على البيئة والسياحة والتنمية المستدامة والمتوازنة.

كما يقتضي تسليط الضوء على خلو القانون الجديد من أي حوافز أو تعويض محق للأشخاص الطبيعيِّين والمعنويِّين الذين تضامنوا ووضعوا مؤسساتهم وإمكانياتهم بتصرّف النازحين والمتضرّرين مع تقديم العون والمساعدة والإحاطة والخدمات خلال كل فترة الأحداث، كما وهؤلاء المستعدّون للتبرّع والمساعدة خلال فترة إعادة الإعمار والترميم الآتية.

إذاً، لا يجوز أن تقتصر الحوافز والإعفاءات على الإعفاء من الرسوم والضرائب التي تطال المتضرّر المستفيد من المساعدة فحسب، كالرسوم الجمركية والضريبة على القيمة المضافة كما هو ملحوظ في القانون الجديد، بل يقتضي أيضاً أن تشمل الإعفاءات رسوم الإنتقال بالنسبة إلى المتضرّرين أنفسهم، الملحوظة في المادتَين 16 و44 من المرسوم الاشتراعي رقم 146 تاريخ 12/6/1959 وتعديلاته (قانون رسم الإنتقال)، كما وحق التنزيل من الأرباح بالنسبة إلى الجهة المتضامنة المساعدة أو الواهبة عملاً بأحكام البند التاسع من المادة السابعة من المرسوم الإشتراعي رقم 144 تاريخ 12 حزيران 1959 (قانون ضريبة الدخل) والمادة 1 من المرسوم رقم 14913 الصادر في 17/7/1970، المعدّل بموجب المرسوم رقم 1785 تاريخ 14/2/1979، والمتضمّن تعيين الحدود العامة لنفقات الإسعاف التي يمكن تنزيلها من الأرباح الخاضعة إلى ضريبة الدخل.

وكان جديراً بالسلطتَين التنفيذية والتشريعية إبداء التقدير والتنويه بهكذا تصرّف وطني تضامني المُحصِّن للوحدة الوطنية والعقد الإجتماعي الجامع بين المواطنين، والذي يُعتبر قدوة يقتضي الإحتذاء بها في أي ظرف أو حين. وبالمقارنة مع ما تضمّنه القانون رقم 194/2020 بالشأن عينه، يتبيّن من جهة أولى أنّ المادة السادسة (أولاً) منه قد نصّت على ما حرفيّته: «خلافاً لأي نص آخر، يُعتبر مقبولاً التنزيل من واردات المؤسسات الخاضعة للتكليف بضريبة الدخل على أساس الربح الحقيقي، المبالغ التي تدفعها تلك المؤسسات على سبيل التبرّع بقصد مساعدة المكلّفين أو المواطنين المتضرّرين، وذلك اعتباراً من 5/8/2020 ولغاية 31/12/2021، سواء حصل التبرّع مباشرة إلى المتضرّرين، أو حصل بشكل غير مباشر من خلال التبرّع إلى مؤسسات وهيئات ومنظمات وجمعيات تقوم هي بدفعها إلى هؤلاء المتضرّرين، أو تستعملها لتمويل عمليات ترميم وإعادة إعمار ممتلكاتهم ومؤسساتهم ومنازلهم، وذلك ضمن حدّ أقصى يساوي أرباح السنة التي حصل خلالها التبرّع، على أن تكون مثبّتة بمستندات يمكن الركون إليها». كما نصّ البند خامساً من المادة السادسة من القانون عينه رقم 194/2020 على أنّه «وخلافاً لأحكام المادتَين 16 و44 من المرسوم الاشتراعي رقم 146 تاريخ 12/6/1959 وتعديلاته (قانون رسم الانتقال) وأي نص آخر، تُعفى من رسوم الانتقال، جميع المساعدات والهبات والتبرّعات العينية والنقدية، التي يثبت أنّها دفعت على سبيل الإسعاف أو التبرّع أو الإحسان إلى الجمعيات والهيئات والطوائف وسائر أشخاص القانون الخاص والأشخاص الطبيعيِّين المتضرِّرين لتجاوز الأضرار الناتجة من انفجار مرفأ بيروت، مهما كان حجمها ومن دون تطبيق الشطور أو الحدود القصوى التي تلحظها المواد المذكورة، على أن تكون مثبتة بمستندات يمكن الركون إليها».

بالتالي، وفي حال لم يُعدَّل القانون الجديد ليتضمّن أحكاماً صريحة مماثلة، فهناك خطر أن يُكلَّف الأشخاص المتضرّرون المستفيدون من المساعدات والهبات برسوم إنتقال بأعلى نسبة ملحوظة في القانون (45%) نظراً لإنتفاء رابط القرابة مع الجهة الواهبة أو المانحة. وبالتالي، يخسرون ضريبياً ما يكونون قد حصلوا عليه هبةً.

وأخيراً وليس آخراً، تلحظ المادة الثامنة من القانون الجديد إعفاءً من رسم الإنتقال لمصلحة ورثة اللبنانيِّين «الذين استشهدوا أو يَستشهدون بتاريخ لاحق لصدور هذا القانون، من جرّاء الحرب الإسرائيلية على الأراضي اللبنانية وذلك، على جميع الحقوق والأموال المنقولة وغير المنقولة المتعلقة بتركات مورثهم». كما ويطال الإعفاء عينه بوالص التأمين على الحياة. وعليه، وبقدر ما هو طبيعي ومنطقي إعفاء ورثة الذين سبق واستشهدوا خلال الحرب، إلّا أنّ إبقاء الإعفاء مفتوحاً من دون تحديد مدة زمنية معيّنة (وإن كان ذلك مفهوماً نظراً لتمادي واستمرار العدوان) من شأنه أن يخلق حالة من عدم اليَقين والإستقرار التي لا تسوغها المبادئ القانونية والدستورية المرعية الإجراء. وبالتالي، من الأفضل بين حين والآخر تعديل النص إذا إقتضى الأمر وتمديد فترة الإعفاء.

وفي الختام، لا يسعَ المراقب إلّا أن يُعجَب ويتعجّب ويقلق لحجم الخفة والإستهتار والعجز في صياغة ومناقشة وإقرار القوانين من قِبل المشرّعين اللبنانيِّين. وبالتالي، فإن كانت الشوائب والأخطاء والمطبّات المفصّلة أعلاه مقصودة، فهذه مشكلة تسدعي الريبة والتحرّك السريع. أمّا إذا كانت غير مقصودة، فالمشكلة أعظم وتستدعي إعادة النظر في العديد من الأمور… بدءاً بممثلي الشعب.

Extension of the 2024 Built property tax filling deadline till the 31 July 2025

The Ministry of Finance decision #615/1 dated 1st July 2025 (attached a scanned copy) extended the deadline for the built property tax filling of the year 2024 and the payment of the related due tax until the 31st July 2025.

MoF answers to the LACPA questions on the Law #330

Here is the Ministry of Finance (MoF) answers to the Lebanese Association of Certified Public Accountant (LACPA) questions on the Law # 330 dated 4/12/2024 (attached a scanned copy) and its MoF application decisions #338/1, 339/1 and 340/1 related to the Exceptional Revaluation of Fixed Assets, Inventory and Foreign Exchange adjustment of the LBP Devaluation effect on receivables, payables and cash & bank accounts from the year 2022 till the 31st December 2026.

The major clarification we were waiting for was in relation with the Foreign Exchange adjustment of the LBP Devaluation effect on receivables, payables and cash & bank accounts at the opening of the year 2022. The MoF has clarified in the last page of its answers, that the positive differences of exchange up to 15,000 LBP/USD are subject to income tax and the negative differences of exchange can be deducted from the taxable income, while any difference of exchange from 15,000 LBP/USD to 42,000 LBP/USD as at 31 December 2022 and then to 89,500 LBP/USD as at 31 December 2023 are not subject to income tax (i.e. positive and negative differences of exchange should be reverted while transiting from the accounting result to the taxable result).

MoF decision #583/1 dated 23 June 2025 – Reductions on tax penalties till 30 September 2025

The Ministry of Finance (MoF) decision # 583/1 dated 23 June 2024 (attached a scanned copy) has granted rebates on tax penalties on tax adjustments (whether issued and notified by the MoF or not yet issued) till the 30th September 2025.

MoF decision #582/1 dated 23 June 2025 – Application mechanism for forensic audit on subsidized USD exchange rate

The Ministry of Finance (MoF) decision # 582/1 dated 23 June 2025 (attached a scanned copy) has set the joint mechanism between the Ministry of Justice and the Ministry of Finance in application of the Law # 240 dated 16th July 2021 that imposed an external forensic audit on all the persons that benefited from the subsidized US Dollar exchange rate or its equivalent in Lebanese Pounds.

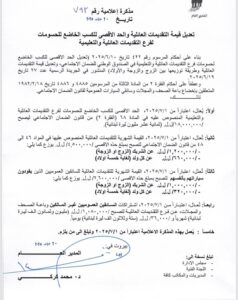

Decree #422 dated 10 June 2025 increasing the value of the NSSF family allowances

Decree #422 dated 10th June 2025, published in the Official Gazette #27 on the 19th June 2025:

1) The monthly salary ceiling subject to the family allowance of 6% has increased to LBP 18,000,000.

2) The value of the monthly family allowances have increased to a maximum of LBP 4,500,000 being:

a. LBP 1,200,000 for the partner (spouse or husband)

b. and LBP 660,000 for each child (up to maximum 5 children).

This increase will be in force starting from the month that follows its publication in the Official Gazette.

NSSF Notification #793 dated 20 June 2025 specifies that this Decree will be in force starting from the 1st July 2025.

Extension of several tax filling deadlines

MoF decision #545/1: Extension of the deadline for the electronic tax filing of the income from foreign movable assets for the fiscal year 2024 according to the article 82 of the Income Tax Law till the 30th June 2025 inclusive.

MoF decision #546/1: Extension of the deadline for the filling of the annual declaration forms (including the UBO M18 form) for the year 2024 for taxpayers subject to tax on a real profit basis (sole proprietorships, partnerships and institutions who are exempt from income tax and adopting the accrual basis of accounting) and the payment of the related tax as well as for submitting the annual non-resident tax (G5 form) due as per article 41 and 42 of the income tax law till the 29th August 2025 inclusive.

MoF decision #547/1: Extension of the deadline for the annual tax on salaries declarations (R5,R6,R7) of the year 2024 and the payment of the related due tax till the 29th August 2025 inclusive